Bankroll Management with Keeks: Strategy Comparison

In this final post of our series on bankroll management strategies in Keeks, we’ll bring everything together with a comparison of all the approaches we’ve explored. We’ll help you understand which strategy might be best for your specific situation, risk tolerance, and goals.

Recap of Bankroll Management Strategies

Over the course of this series, we’ve explored eight different bankroll management strategies:

- Kelly Criterion - The mathematically optimal strategy for maximizing long-term growth

- Fractional Kelly - A more conservative version of Kelly that reduces volatility

- Drawdown-Adjusted Kelly - A dynamic Kelly variant that adjusts bet sizing based on drawdowns

- OptimalF - Ralph Vince’s approach that maximizes geometric growth based on historical results

- Fixed Fraction - A simple strategy that bets a constant percentage of the bankroll

- CPPI - A floor-based approach that protects a minimum bankroll value

- Dynamic Bankroll Management - An adaptive approach that adjusts bet sizing based on recent performance

- Naive Strategy - The simplest approach that bets a fixed amount regardless of bankroll size

Each strategy has its own strengths, weaknesses, and ideal use cases. Let’s compare them across several key dimensions.

Head-to-Head Comparison

Let’s run a comprehensive simulation to compare all strategies under identical conditions:

import numpy as np

from keeks.bankroll import BankRoll

from keeks.binary_strategies.kelly import KellyCriterion, FractionalKelly, DrawdownAdjustedKelly

from keeks.binary_strategies.optimalf import OptimalF

from keeks.binary_strategies.fixed_fraction import FixedFraction

from keeks.binary_strategies.cppi import CPPI

from keeks.binary_strategies.dynamic import DynamicBankrollManagement

from keeks.binary_strategies.naive import NaiveStrategy

from keeks.simulators.repeated_binary import RepeatedBinarySimulator

import matplotlib.pyplot as plt

# Set up our simulation parameters

win_probability = 0.55

payoff = 1.0

loss = 1.0

trials = 1000

initial_funds = 1000.0

# Generate historical data for OptimalF

np.random.seed(42)

historical_trials = 200

historical_results = np.random.choice(

[payoff, -loss],

size=historical_trials,

p=[win_probability, 1-win_probability]

)

# Calculate the Kelly fraction for reference

kelly = KellyCriterion(payoff=payoff, loss=loss)

kelly_fraction = kelly.calculate_bet_fraction(win_probability)

print(f"Kelly fraction for this scenario: {kelly_fraction:.4f}")

print(f"Initial Kelly bet: ${kelly_fraction * initial_funds:.2f}")

# Create all strategies

strategies = {

"Kelly": KellyCriterion(payoff=payoff, loss=loss),

"Half Kelly": FractionalKelly(payoff=payoff, loss=loss, fraction=0.5),

"Quarter Kelly": FractionalKelly(payoff=payoff, loss=loss, fraction=0.25),

"Drawdown-Adjusted Kelly (20%)": DrawdownAdjustedKelly(payoff=payoff, loss=loss, max_drawdown=0.2),

"OptimalF": OptimalF(historical_returns=historical_results),

"Fixed Fraction (3%)": FixedFraction(fraction=0.03),

"CPPI (Floor: 80%, m=3)": CPPI(floor=0.8*initial_funds, multiplier=3),

"Dynamic (±50%, 5 lookback)": DynamicBankrollManagement(

base_fraction=0.03, max_increase=0.5, max_decrease=0.5, lookback_period=5

),

"Naive ($10)": NaiveStrategy(bet_amount=10.0)

}

# Create a simulator with fixed random seed for fair comparison

simulator = RepeatedBinarySimulator(

payoff=payoff,

loss=loss,

probability=win_probability,

trials=trials,

random_seed=43 # Different seed from historical data

)

# Run simulations

results = {}

for name, strategy in strategies.items():

bankroll = BankRoll(initial_funds=initial_funds)

simulator.evaluate_strategy(strategy, bankroll)

results[name] = {

"history": bankroll.history.copy(),

"drawdowns": bankroll.drawdown_history.copy()

}

# Plot the bankroll histories

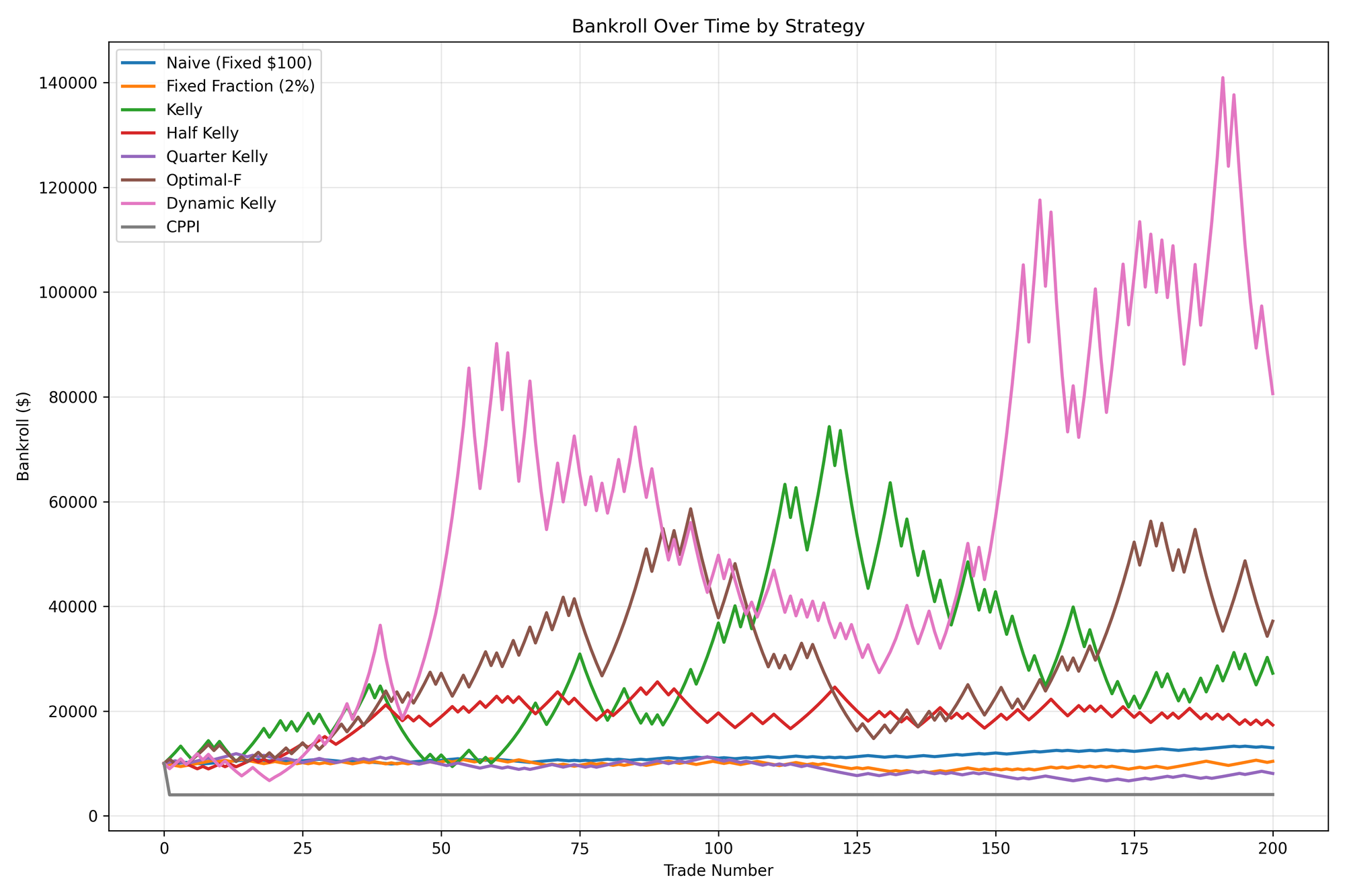

plt.figure(figsize=(15, 10))

for name, data in results.items():

plt.plot(data["history"], label=name)

plt.title('Comparison of All Bankroll Management Strategies')

plt.xlabel('Number of Bets')

plt.ylabel('Bankroll Size')

plt.legend()

plt.grid(True)

plt.show()

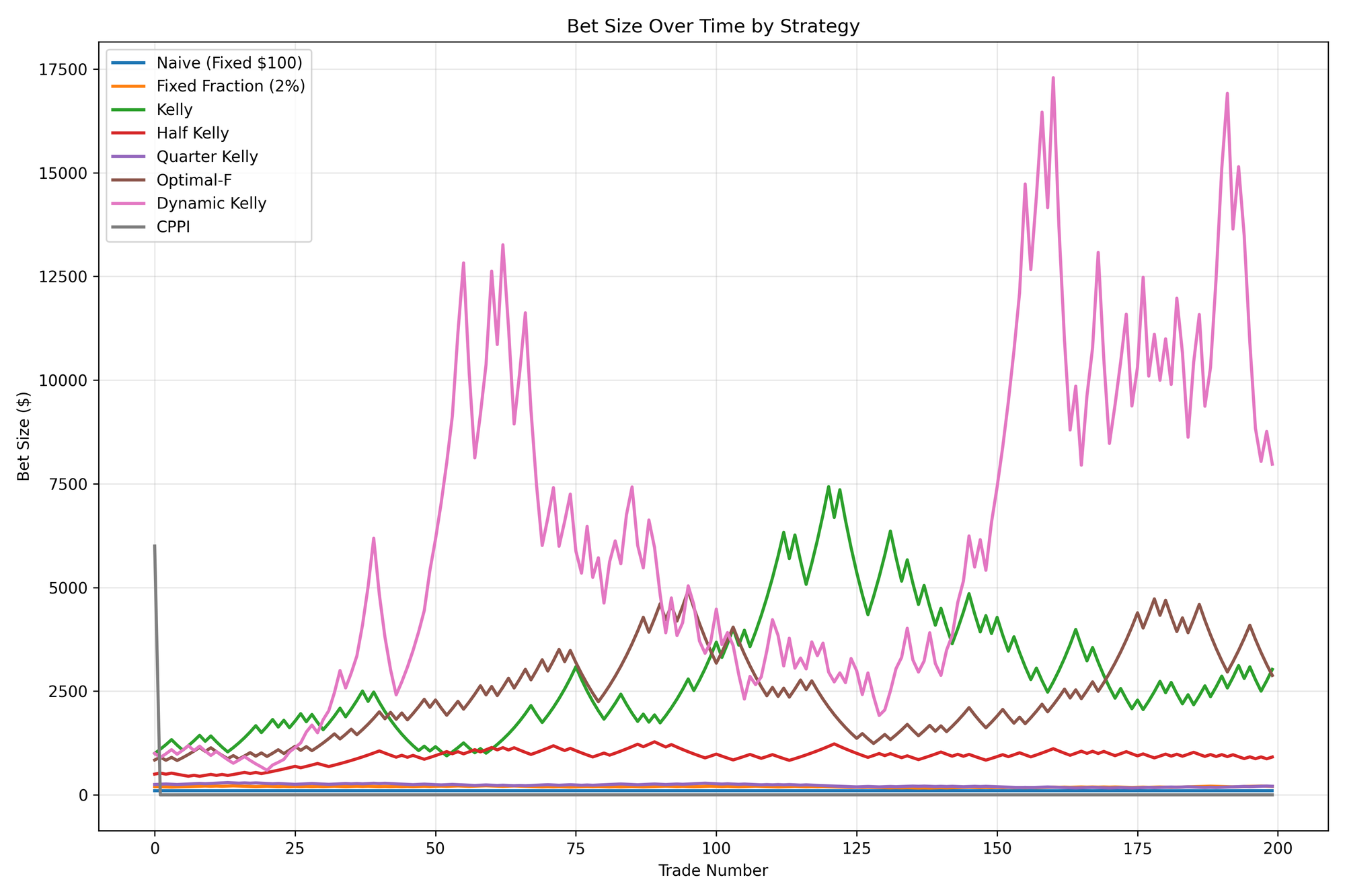

# Plot the drawdown histories

plt.figure(figsize=(15, 10))

for name, data in results.items():

plt.plot(data["drawdowns"], label=name)

plt.title('Drawdown Comparison of All Strategies')

plt.xlabel('Number of Bets')

plt.ylabel('Drawdown (%)')

plt.legend()

plt.grid(True)

plt.show()

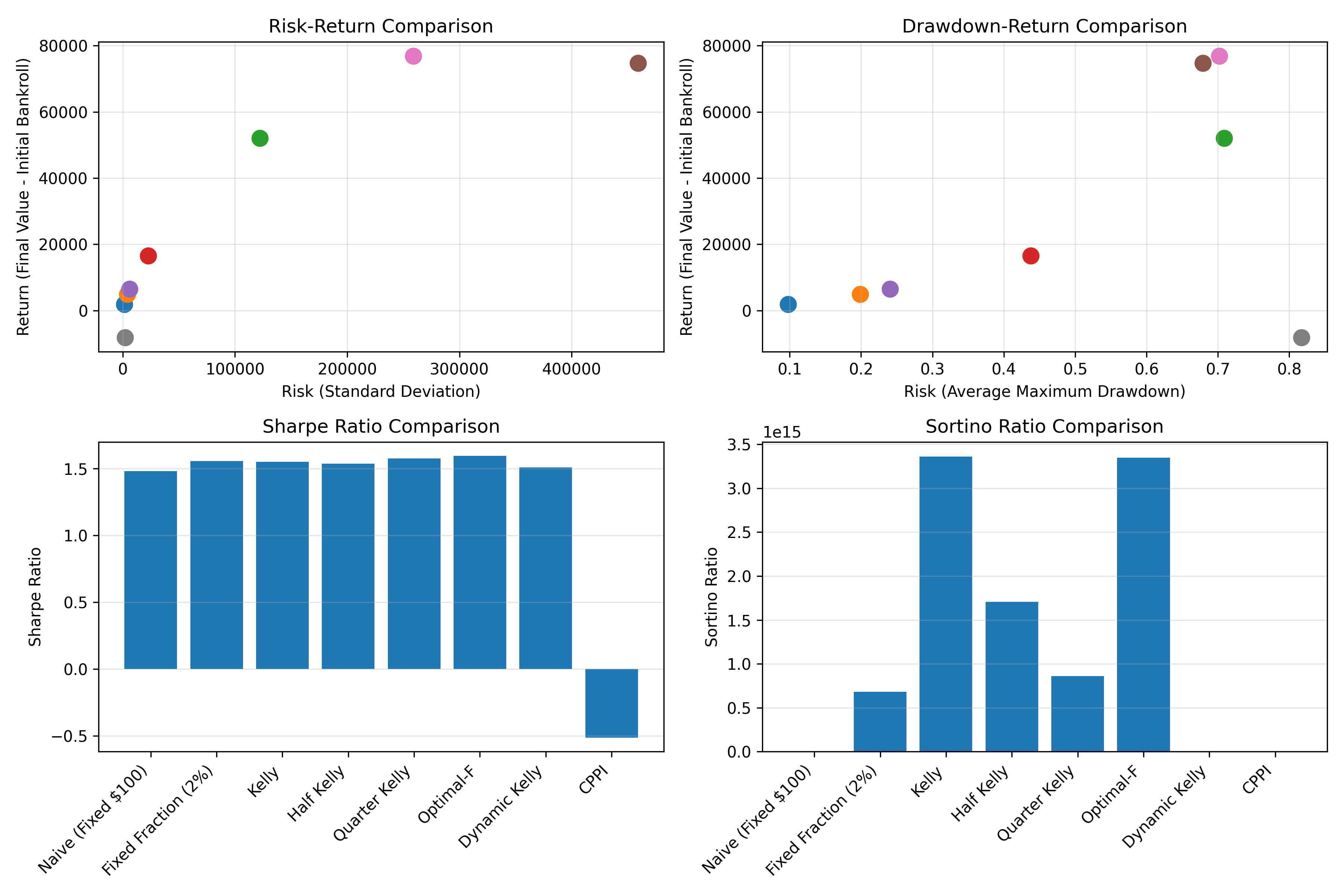

# Calculate and display statistics

stats = []

for name, data in results.items():

history = data["history"]

drawdowns = data["drawdowns"]

final_value = history[-1]

max_value = max(history)

min_value = min(history)

max_drawdown = max(drawdowns) * 100

growth_rate = (final_value / initial_funds) ** (1 / trials) - 1

total_return = (final_value / initial_funds - 1) * 100

stats.append({

"Strategy": name,

"Final Bankroll": final_value,

"Total Return": total_return,

"Growth Rate": growth_rate * 100, # Convert to percentage

"Max Drawdown": max_drawdown,

"Min Bankroll": min_value

})

print(f"{name}:")

print(f" Final bankroll: ${final_value:.2f}")

print(f" Total return: {total_return:.2f}%")

print(f" Growth rate: {growth_rate:.2%} per bet")

print(f" Maximum drawdown: {max_drawdown:.2f}%")

print(f" Minimum bankroll: ${min_value:.2f}")

print()

# Create a comparison table

import pandas as pd

df = pd.DataFrame(stats)

df = df.set_index('Strategy')

df = df.sort_values('Final Bankroll', ascending=False)

print("Strategy Comparison Table (Sorted by Final Bankroll):")

print(df.round(2))

Strategy Comparison Table

Here’s a summary of how each strategy performs across key metrics:

| Strategy | Growth Potential | Drawdown Risk | Complexity | Psychological Comfort | When to Use |

|---|---|---|---|---|---|

| Kelly Criterion | Excellent | High | Moderate | Low | When maximizing long-term growth is the only goal |

| Fractional Kelly | Very Good | Moderate | Moderate | Moderate | For a balance of growth and risk management |

| Drawdown-Adjusted Kelly | Good | Low-Moderate | High | Good | When protecting against drawdowns is important |

| OptimalF | Excellent | High | High | Low | When you have good historical data but uncertain probabilities |

| Fixed Fraction | Good | Moderate | Low | Good | For simplicity and consistency |

| CPPI | Moderate | Very Low | Moderate | Excellent | When capital preservation is critical |

| Dynamic Bankroll Management | Good-Very Good | Moderate | High | Moderate | In streaky environments or with varying edge |

| Naive Strategy | Low-Moderate | High | Very Low | Excellent | For beginners or as a baseline |

Choosing the Right Strategy for You

Selecting the optimal bankroll management strategy depends on several factors:

1. Your Risk Tolerance

- Low Risk Tolerance: Consider CPPI, Quarter Kelly, or Drawdown-Adjusted Kelly

- Moderate Risk Tolerance: Half Kelly, Fixed Fraction, or Dynamic Bankroll Management

- High Risk Tolerance: Full Kelly or OptimalF

2. Your Betting Experience

- Beginners: Start with Naive Strategy or Fixed Fraction

- Intermediate: Progress to Half Kelly or CPPI

- Advanced: Full Kelly, OptimalF, or Dynamic Bankroll Management

3. Your Primary Goal

- Maximum Growth: Kelly Criterion or OptimalF

- Capital Preservation: CPPI or Drawdown-Adjusted Kelly

- Balanced Approach: Fractional Kelly or Fixed Fraction

- Adaptability: Dynamic Bankroll Management

4. Your Betting Environment

- Stable Edge: Kelly Criterion or Fractional Kelly

- Varying Edge: Dynamic Bankroll Management

- Streaky Markets: Dynamic Bankroll Management or Drawdown-Adjusted Kelly

- Unknown Probabilities: OptimalF or Fixed Fraction

Real-World Scenario Analysis

Let’s examine how different strategies might perform in various real-world scenarios:

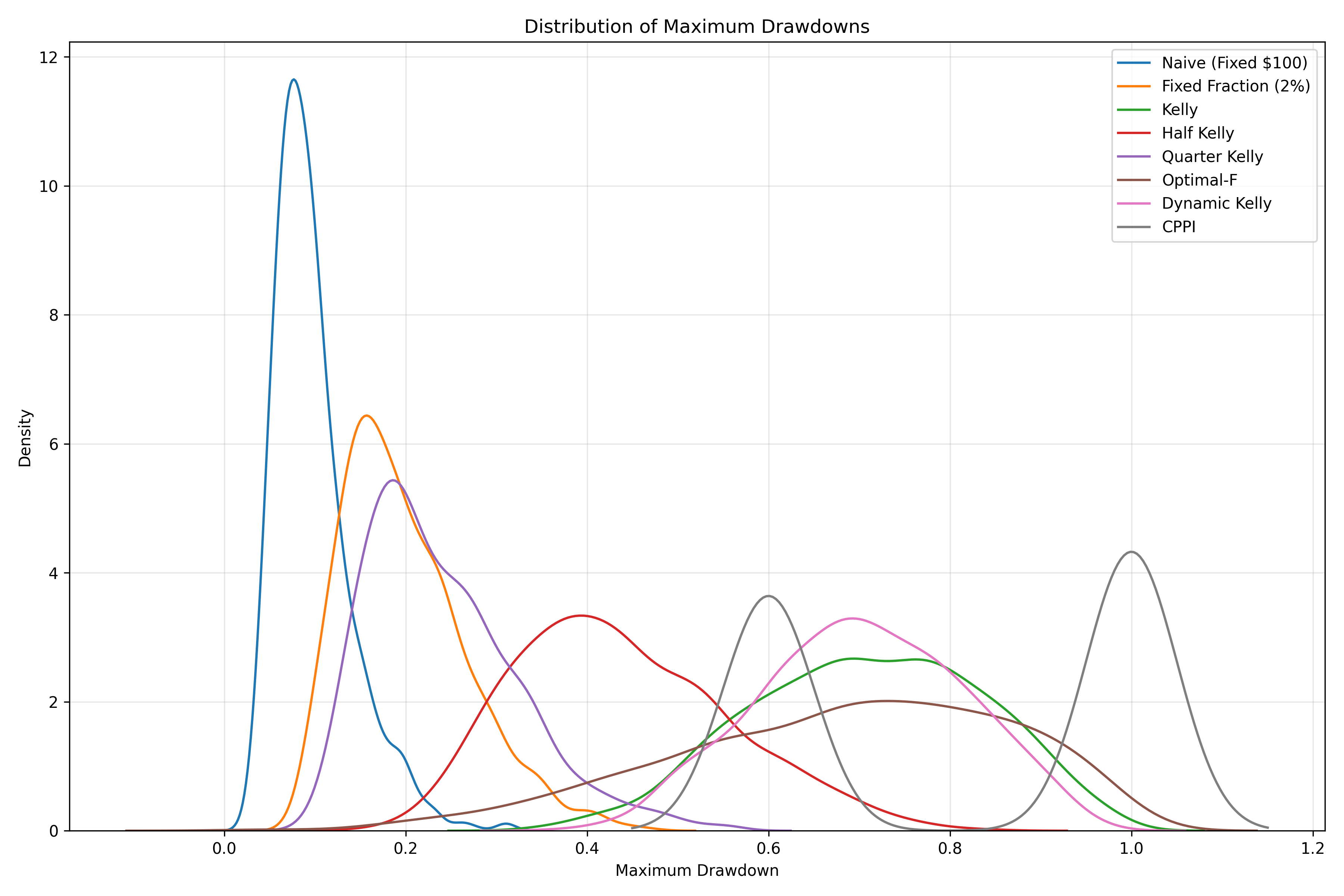

Scenario 1: Sports Betting with a Small Edge

from keeks.bankroll import BankRoll

from keeks.binary_strategies.kelly import KellyCriterion, FractionalKelly

from keeks.binary_strategies.fixed_fraction import FixedFraction

from keeks.binary_strategies.naive import NaiveStrategy

import numpy as np

import matplotlib.pyplot as plt

# Scenario: Sports betting with standard -110 odds and a 53% win rate

win_probability = 0.53

payoff = 0.91 # -110 odds: bet $110 to win $100

loss = 1.0

initial_funds = 1000.0

num_bets = 500

# Create strategies

kelly = KellyCriterion(payoff=payoff, loss=loss)

half_kelly = FractionalKelly(payoff=payoff, loss=loss, fraction=0.5)

fixed_fraction = FixedFraction(fraction=0.02)

naive = NaiveStrategy(bet_amount=20.0)

# Calculate Kelly fraction

kelly_fraction = kelly.calculate_bet_fraction(win_probability)

print(f"Kelly fraction for sports betting with 53% win rate: {kelly_fraction:.4f}")

# Generate a sequence of bets

np.random.seed(42)

results = np.random.choice([1, -1], size=num_bets, p=[win_probability, 1-win_probability])

# Simulate each strategy

strategies = {

"Kelly": kelly,

"Half Kelly": half_kelly,

"Fixed Fraction (2%)": fixed_fraction,

"Naive ($20)": naive

}

bankroll_histories = {}

for name, strategy in strategies.items():

bankroll = BankRoll(initial_funds=initial_funds)

for result in results:

if hasattr(strategy, 'calculate_bet_fraction'):

bet_fraction = strategy.calculate_bet_fraction(win_probability)

bet_amount = bet_fraction * bankroll.current_funds

else:

bet_amount = strategy.bet_amount

if result == 1:

# Win

profit = bet_amount * payoff

bankroll.update(profit)

else:

# Loss

bankroll.update(-bet_amount)

bankroll_histories[name] = bankroll.history.copy()

# Plot the results

plt.figure(figsize=(12, 8))

for name, history in bankroll_histories.items():

plt.plot(history, label=name)

plt.title('Sports Betting Scenario: 53% Win Rate, -110 Odds')

plt.xlabel('Number of Bets')

plt.ylabel('Bankroll Size')

plt.legend()

plt.grid(True)

plt.show()

# Calculate final statistics

for name, history in bankroll_histories.items():

final_value = history[-1]

max_value = max(history)

min_value = min(history)

max_drawdown = (max_value - min_value) / max_value * 100

total_return = (final_value / initial_funds - 1) * 100

print(f"{name}:")

print(f" Final bankroll: ${final_value:.2f}")

print(f" Total return: {total_return:.2f}%")

print(f" Maximum drawdown: {max_drawdown:.2f}%")

print()

Scenario 2: Investment Portfolio with Varying Market Conditions

from keeks.bankroll import BankRoll

from keeks.binary_strategies.kelly import FractionalKelly

from keeks.binary_strategies.cppi import CPPI

from keeks.binary_strategies.dynamic import DynamicBankrollManagement

import numpy as np

import matplotlib.pyplot as plt

# Scenario: Investment portfolio with changing market conditions

initial_funds = 100000.0

months = 60 # 5 years

# Create strategies

half_kelly = FractionalKelly(payoff=0.15, loss=0.10, fraction=0.5) # 15% gain, 10% loss

cppi = CPPI(floor=0.9*initial_funds, multiplier=3)

dynamic = DynamicBankrollManagement(base_fraction=0.3, max_increase=0.5, max_decrease=0.5, lookback_period=3)

# Generate market conditions with regime changes

np.random.seed(42)

# Bull market (first 24 months): 65% chance of 15% gain, 35% chance of 10% loss

# Bear market (next 12 months): 40% chance of 15% gain, 60% chance of 10% loss

# Recovery (last 24 months): 55% chance of 15% gain, 45% chance of 10% loss

probabilities = np.concatenate([

np.ones(24) * 0.65, # Bull market

np.ones(12) * 0.40, # Bear market

np.ones(24) * 0.55 # Recovery

])

# Simulate each strategy

strategies = {

"Half Kelly": half_kelly,

"CPPI (Floor: 90%, m=3)": cppi,

"Dynamic (±50%, 3 lookback)": dynamic

}

bankroll_histories = {}

allocation_histories = {}

for name, strategy in strategies.items():

bankroll = BankRoll(initial_funds=initial_funds)

allocations = []

for i in range(months):

# Current market regime

win_probability = probabilities[i]

# Calculate allocation

if hasattr(strategy, 'calculate_bet_fraction'):

if name == "Dynamic (±50%, 3 lookback)":

# For dynamic strategy, look at recent performance

lookback = min(i, strategy.lookback_period)

recent_results = []

for j in range(lookback):

idx = i - j - 1

if idx >= 0:

recent_win = np.random.random() < probabilities[idx]

recent_results.append(1 if recent_win else -1)

bet_fraction = strategy.calculate_bet_fraction(recent_results)

else:

bet_fraction = strategy.calculate_bet_fraction(win_probability)

allocation = bet_fraction * bankroll.current_funds

elif hasattr(strategy, 'calculate_bet_amount'):

allocation = strategy.calculate_bet_amount(bankroll.current_funds)

allocations.append(allocation)

# Determine if we win or lose this month

win = np.random.random() < win_probability

if win:

# Gain

profit = allocation * 0.15 # 15% gain

bankroll.update(profit)

else:

# Loss

loss = allocation * 0.10 # 10% loss

bankroll.update(-loss)

bankroll_histories[name] = bankroll.history.copy()

allocation_histories[name] = allocations

# Plot the results

fig, (ax1, ax2) = plt.subplots(2, 1, figsize=(12, 12), sharex=True)

# Plot the bankroll

for name, history in bankroll_histories.items():

ax1.plot(history, label=name)

ax1.axvspan(24, 36, alpha=0.2, color='red', label='Bear Market')

ax1.set_title('Investment Portfolio with Changing Market Conditions')

ax1.set_ylabel('Portfolio Value ($)')

ax1.legend()

ax1.grid(True)

# Plot the allocations

for name, allocations in allocation_histories.items():

ax2.plot(allocations, label=f"{name} Allocation")

ax2.axvspan(24, 36, alpha=0.2, color='red')

ax2.set_title('Investment Allocations Over Time')

ax2.set_xlabel('Month')

ax2.set_ylabel('Allocation Amount ($)')

ax2.legend()

ax2.grid(True)

plt.tight_layout()

plt.show()

# Calculate final statistics

for name, history in bankroll_histories.items():

final_value = history[-1]

max_value = max(history)

min_value = min(history)

max_drawdown = (max_value - min_value) / max_value * 100

total_return = (final_value / initial_funds - 1) * 100

annualized_return = ((1 + total_return/100) ** (12/months) - 1) * 100

print(f"{name}:")

print(f" Final portfolio: ${final_value:.2f}")

print(f" Total return: {total_return:.2f}%")

print(f" Annualized return: {annualized_return:.2f}%")

print(f" Maximum drawdown: {max_drawdown:.2f}%")

print()

Implementing Your Strategy with Keeks

Now that you understand the different strategies and their trade-offs, let’s look at how to implement your chosen approach with Keeks:

from keeks.bankroll import BankRoll

from keeks.binary_strategies.kelly import FractionalKelly

from keeks.simulators.repeated_binary import RepeatedBinarySimulator

import matplotlib.pyplot as plt

# Example: Implementing Half Kelly for sports betting

# Create a bankroll with initial funds

bankroll = BankRoll(initial_funds=1000.0, max_draw_down=0.3)

# Create a Half Kelly strategy for standard -110 odds

half_kelly = FractionalKelly(payoff=0.91, loss=1.0, fraction=0.5)

# For a specific bet with a 54% chance of winning

win_probability = 0.54

bet_fraction = half_kelly.calculate_bet_fraction(win_probability)

bet_amount = bet_fraction * bankroll.current_funds

print(f"Bankroll: ${bankroll.current_funds:.2f}")

print(f"Win probability: {win_probability:.0%}")

print(f"Half Kelly fraction: {bet_fraction:.4f}")

print(f"Recommended bet: ${bet_amount:.2f}")

# Simulate future performance

simulator = RepeatedBinarySimulator(

payoff=0.91,

loss=1.0,

probability=win_probability,

trials=500

)

# Run the simulation

simulator.evaluate_strategy(half_kelly, bankroll)

# Plot the results

plt.figure(figsize=(10, 6))

plt.plot(bankroll.history)

plt.title('Projected Bankroll Growth Using Half Kelly')

plt.xlabel('Number of Bets')

plt.ylabel('Bankroll Size')

plt.grid(True)

plt.show()

# Print final results

final_bankroll = bankroll.history[-1]

total_return = (final_bankroll / 1000.0 - 1) * 100

print(f"After 500 bets:")

print(f" Final bankroll: ${final_bankroll:.2f}")

print(f" Total return: {total_return:.2f}%")

Combining Strategies for Optimal Results

In practice, many professional bettors and investors use a combination of strategies to get the best of all worlds. Here are some hybrid approaches to consider:

- Kelly-CPPI Hybrid: Use Kelly to determine your bet size, but never let your bankroll fall below a predetermined floor (like CPPI)

- Dynamic Fractional Kelly: Use Fractional Kelly as your base strategy, but adjust the fraction based on recent performance (like Dynamic Bankroll Management)

- Tiered Approach: Use different strategies for different types of bets based on your confidence level

Here’s an example of a Kelly-CPPI hybrid:

from keeks.bankroll import BankRoll

from keeks.binary_strategies.kelly import KellyCriterion

import numpy as np

import matplotlib.pyplot as plt

# Create a hybrid Kelly-CPPI strategy

class KellyCPPIHybrid:

def __init__(self, payoff, loss, floor_percentage=0.8):

self.kelly = KellyCriterion(payoff=payoff, loss=loss)

self.floor_percentage = floor_percentage

self.initial_bankroll = None

def calculate_bet_amount(self, bankroll, win_probability):

# Set initial bankroll if not already set

if self.initial_bankroll is None:

self.initial_bankroll = bankroll

# Calculate floor

floor = self.floor_percentage * self.initial_bankroll

# If bankroll is at or below floor, don't bet

if bankroll <= floor:

return 0

# Calculate Kelly bet

kelly_fraction = self.kelly.calculate_bet_fraction(win_probability)

kelly_amount = kelly_fraction * bankroll

# Ensure bet doesn't risk going below floor

max_bet = bankroll - floor

# Return the smaller of Kelly bet and max_bet

return min(kelly_amount, max_bet)

# Simulate the hybrid strategy

initial_funds = 1000.0

bankroll = BankRoll(initial_funds=initial_funds)

hybrid = KellyCPPIHybrid(payoff=1.0, loss=1.0, floor_percentage=0.7)

# Generate a sequence of bets

np.random.seed(42)

num_bets = 500

win_probability = 0.52 # Slightly positive edge

results = np.random.choice([1, -1], size=num_bets, p=[win_probability, 1-win_probability])

# Track our bankroll and bet sizes

bankroll_history = [bankroll.current_funds]

bet_sizes = []

floor = 0.7 * initial_funds

# Simulate the bets

for result in results:

# Calculate the bet size

bet_amount = hybrid.calculate_bet_amount(bankroll.current_funds, win_probability)

bet_sizes.append(bet_amount)

# Apply the result

if result == 1:

# Win

bankroll.update(bet_amount)

else:

# Loss

bankroll.update(-bet_amount)

# Record the new bankroll

bankroll_history.append(bankroll.current_funds)

# Plot the results

plt.figure(figsize=(12, 8))

plt.plot(bankroll_history)

plt.axhline(y=floor, color='r', linestyle='--', label='Floor (70%)')

plt.title('Kelly-CPPI Hybrid Strategy')

plt.xlabel('Number of Bets')

plt.ylabel('Bankroll Size')

plt.legend()

plt.grid(True)

plt.show()

# Plot the bet sizes

plt.figure(figsize=(12, 8))

plt.plot(bet_sizes)

plt.title('Bet Sizes with Kelly-CPPI Hybrid')

plt.xlabel('Bet Number')

plt.ylabel('Bet Size ($)')

plt.grid(True)

plt.show()

# Calculate final statistics

final_bankroll = bankroll_history[-1]

max_bankroll = max(bankroll_history)

min_bankroll = min(bankroll_history)

max_drawdown = (max_bankroll - min_bankroll) / max_bankroll * 100

total_return = (final_bankroll / initial_funds - 1) * 100

print(f"Kelly-CPPI Hybrid Results:")

print(f" Initial bankroll: ${initial_funds:.2f}")

print(f" Final bankroll: ${final_bankroll:.2f}")

print(f" Total return: {total_return:.2f}%")

print(f" Maximum drawdown: {max_drawdown:.2f}%")

print(f" Minimum bankroll: ${min_bankroll:.2f}")

Conclusion: Finding Your Perfect Strategy

After exploring all these bankroll management strategies, the key takeaway is that there’s no one-size-fits-all solution. The best strategy for you depends on your specific circumstances, goals, and psychological makeup.

Here are some final recommendations:

- Start conservative: Begin with a more conservative approach like Half Kelly or Fixed Fraction until you gain confidence

- Monitor and adjust: Regularly review your strategy’s performance and be willing to adjust

- Consider hybrids: Don’t be afraid to combine elements of different strategies

- Stay disciplined: Whatever strategy you choose, stick to it consistently

- Use Keeks: Leverage the Keeks library to implement, test, and refine your approach

Remember that even the most mathematically optimal strategy is only as good as your ability to stick with it. Choose a strategy that not only maximizes your expected returns but also aligns with your risk tolerance and psychological comfort.

Thank you for following this series on bankroll management strategies with Keeks. We hope it helps you make more informed decisions about your betting and investing approach!

Stay in the loop

Get notified when I publish new posts. No spam, unsubscribe anytime.